Description

About the product VALUE FOR MONEY

Group accounting is crucial for ensuring transparency and accuracy in financial reporting across subsidiaries and parent companies. It enables stakeholders to gain a greater understanding of the financial health and performance of the entire group, fostering trust and confidence in the market. This e-product encompasses six essential standards, providing in-depth insights into consolidation, equity method, business combinations, and more, empowering learners to navigate complicated accounting principles with confidence and proficiency.

Unlock the complexities of group accounting standards with our comprehensive Video Lectures and e-Books bundle covering Ind AS 27, Ind AS 28, Ind AS 103, Ind AS 110, Ind AS 111, and Ind AS 112. More than 200+ important topics and concepts have been explained in simple language through practical examples and numerous illustrations. Dive deep into the intricacies of mergers and acquisitions, associates, joint ventures, joint arrangements, and related areas with expert-led tutorials and extensive commentary designed to demystify these critical standards. Live demonstration of how to consolidate Balance Sheet, Statement of Profit and Loss, Other Comprehensive Income, and Statement of Changes in Equity is also included. Elevate your expertise and stay ahead in the world of Ind AS with our holistic e-lectures and e-books.

Covering 6 Standards – Ind AS 27, Ind AS 28, Ind AS 103, Ind AS 110, Ind AS 111 and Ind AS 112

Ind AS 27 – Separate Financial StatementsWhat you will learn:

Ind AS 28 – Investments in Associates and Joint VenturesWhat you will learn:

Ind AS 110 – Consolidated Financial Statements

|

Ind AS 103 – Business Combinations

|

Key features

Subject matter – 200+ important topics and concepts are meticulously discussed in video lectures

Session type – Detailed deliberation on 6 standards with maximum use of practical examples and engaging illustrations

e-Book – 230+ pages of specially curated e-book for thorough understanding

Live conversion – Actual demonstration of how to consolidate a Balance Sheet, PL, OCI and SOCE is included

On-Demand Access – Videos can be accessed anywhere, anytime on any device such as PC, Laptop, Tablet and Mobile

Unlimited Views – There is no restriction to the number of views

Support – Clarification of queries is also offered via digital communication for 1 year from the date of purchase

Study material – Receive an in-depth e-book, presentation slides and a handout of numerical worked examples of all 6 standards

Watch time: 9 hours 17 minutes

About the e-Book

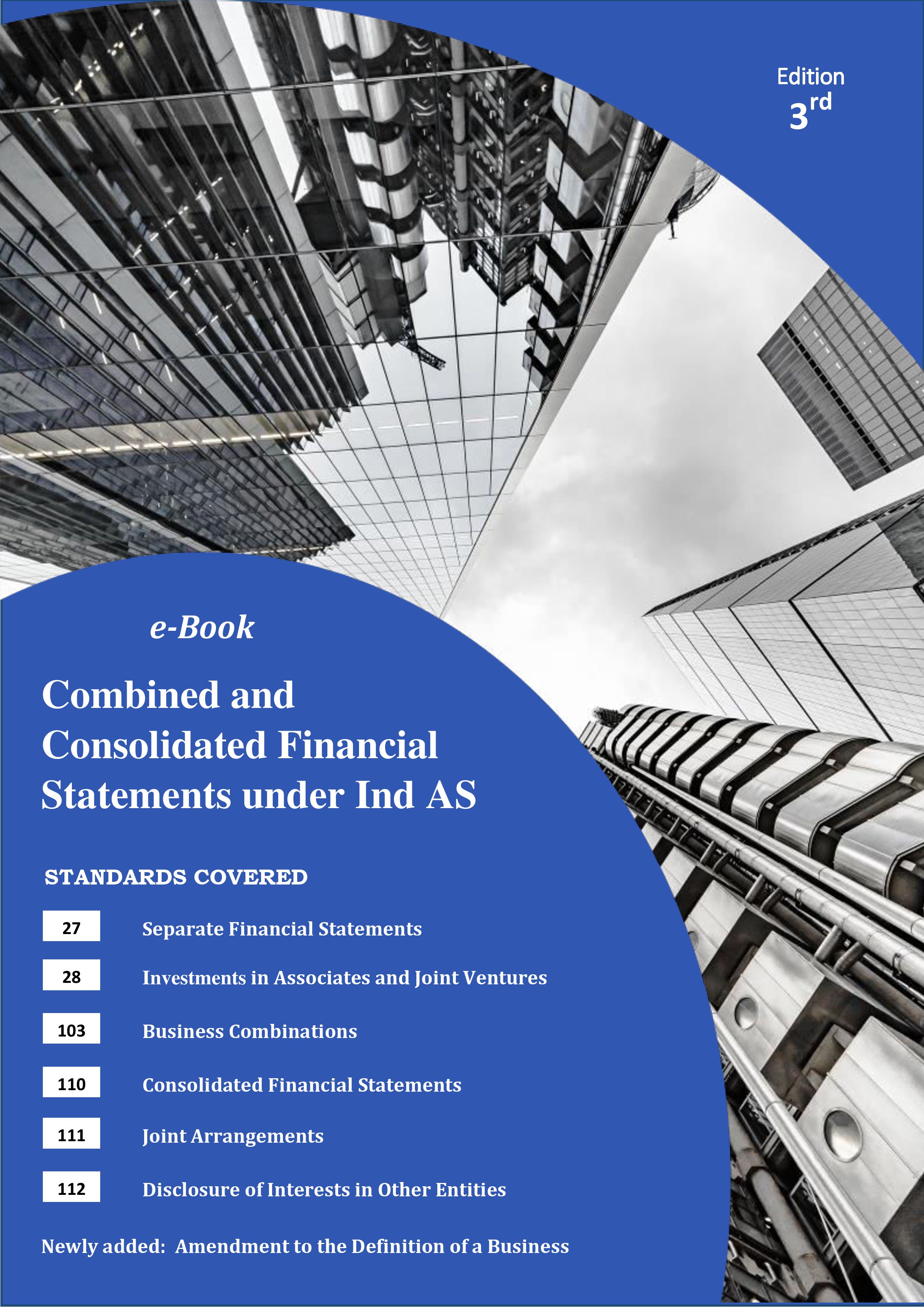

Combined and Consolidated Financial Statements under Ind AS

Consolidation is the ultimate form of accounting. It establishes principles of preparing financial statements of a group in which the assets, liabilities, equity, income, expenses and cash flow of the parent and its subsidiaries are presented as those of a single economic entity. This research based and extensive e-Book contains a high-level technical summary of all 6 standards namely:

- Ind AS 27: Separate Financial Statements

- Ind AS 28: Investments in Associates and Joint Ventures

- Ind AS 103: Business Combinations

- Ind AS 110: Consolidated Financial Statements

- Ind AS 111: Joint Arrangements

- Ind AS 112: Disclosure of Interests in Other Entities

It has been interpreted in detail how these standards are articulated with the use of maximum numerical worked-out examples and case studies. They are further elaborated through exhaustive accounting calculations, journal entries, applicable paragraphs, extracts of financial statements and much more. Moreover, the new Amendment to the Definition of a Business has been included with accurate illustrations.

Pages: 235

Venkatesh R (verified owner) –

the way you have separated the standards and broken down topics with examples and clear explanation is unbelievable. ebook also very helpful in understanding

Nirmal Desai (verified owner) –

This combo pack provides practical insights and interpretations, making them valuable for accounting professionals. Examples are added bonus and language is simple

Kunal Saraf (verified owner) –

if you are looking to understand and apply consolidation and business combination this video plus ebook product is perfect for you

Swarnendu Dutta (verified owner) –

It teaches you everything from the fundamentals to advanced topics…complex concepts are explained in easy to learn manner…will definitely use for future reference

Chandan Sankar (verified owner) –

I must say this was one area i had dificulty for long time thanks to sir lecture I am more comfortable but have to study more and apply at work